Unlocking Export Tax Savings: A Modern Guide to IC-DISCs and How to Use Them Effectively

by

In today’s global marketplace, many U.S. businesses miss a hidden gem of tax savings. Originating in law enacted in 1971, it offers exporters a powerful, but often misunderstood tool for reducing their federal income taxes and freeing up capital for growth. What is this gem? It is the Interest-Charge Domestic International Sales Corporation, commonly known as the IC-DISC.

While the IC-DISC structure has existed for decades, it has regained relevance as one of the few remaining export-incentive tools in the Internal Revenue Code. In essence, an IC-DISC enables a company to convert ordinary income—taxed at rates up to 37% for individuals—into dividend income taxed at preferential capital gains rates, commonly between 15% and 23.8% (inclusive of taxpayers subject to the net investment income tax). Combined with a deductible commission expense at the operating company level, IC-DISCs can create permanent tax savings rather than temporary deferrals. Even after such permanent savings, certain structures can also provide deferral benefits.

Yet, despite its benefits, the IC-DISC remains underutilized because many executives assume it requires significant infrastructure or may otherwise alter customer-facing operations. Except for buy-sell IC-DISCs (which are not common), the reality is that a commission IC-DISC is a paper entity with no employees or office space, operating silently in the background without being involved in day-to-day business operations. The operating business continues manufacturing, shipping, and invoicing customers as usual (but makes commission payments to the IC-DISC internally).

What is an IC-DISC and Why Does It Exist?

An IC-DISC is a U.S. C corporation that makes an election to be treated as an IC-DISC under U.S. tax rules. The C corporation can either be a state law corporation or another type of entity (such as a single-member LLC) that elects corporate classification for federal income tax purposes on Form 8832. To qualify, the entity must file the election to be treated as an IC-DISC on IRS Form 4876-A within 90-days of the beginning of its tax year. Once approved, the entity becomes a tax-exempt export agent for the operating company that exports products (and certain services) to foreign markets.

In the classic structure, the operating/exporting business continues managing sales and operations. The IC-DISC does not need:

- Employees;

- Office space; nor

- Physical involvement in export transactions.

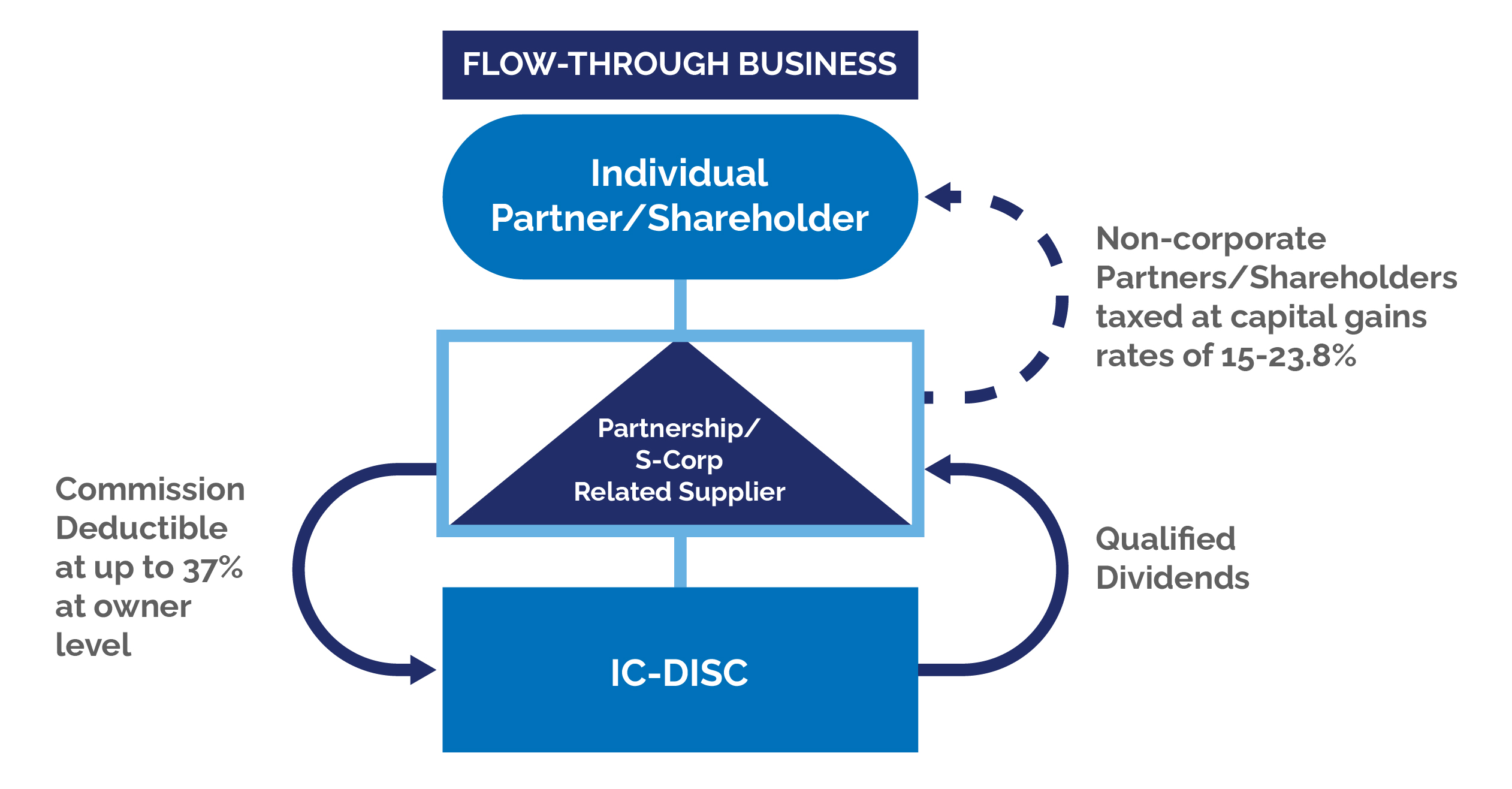

The operating company pays the IC-DISC a commission for export sales. That commission becomes a deduction to the operating company (at either individual rates if it is a partnership or S corporation, or corporate rates if a C corporation) and the resulting commission income of the IC-DISC is not subject to income tax (subject tto limitations discussed below).

Whether in the current year or at some later time, when the IC-DISC distributes its earnings to shareholders in the form of qualified dividends, such income is taxed at favorable capital gains rather than ordinary income rates.

The permanent tax benefit comes from tax rate arbitrage: the commission is deducted at the operating exporter’s ordinary income rate, yet the IC-DISC dividend is taxed at the lower qualified-dividend rate.

Ownership and Structural Flexibility

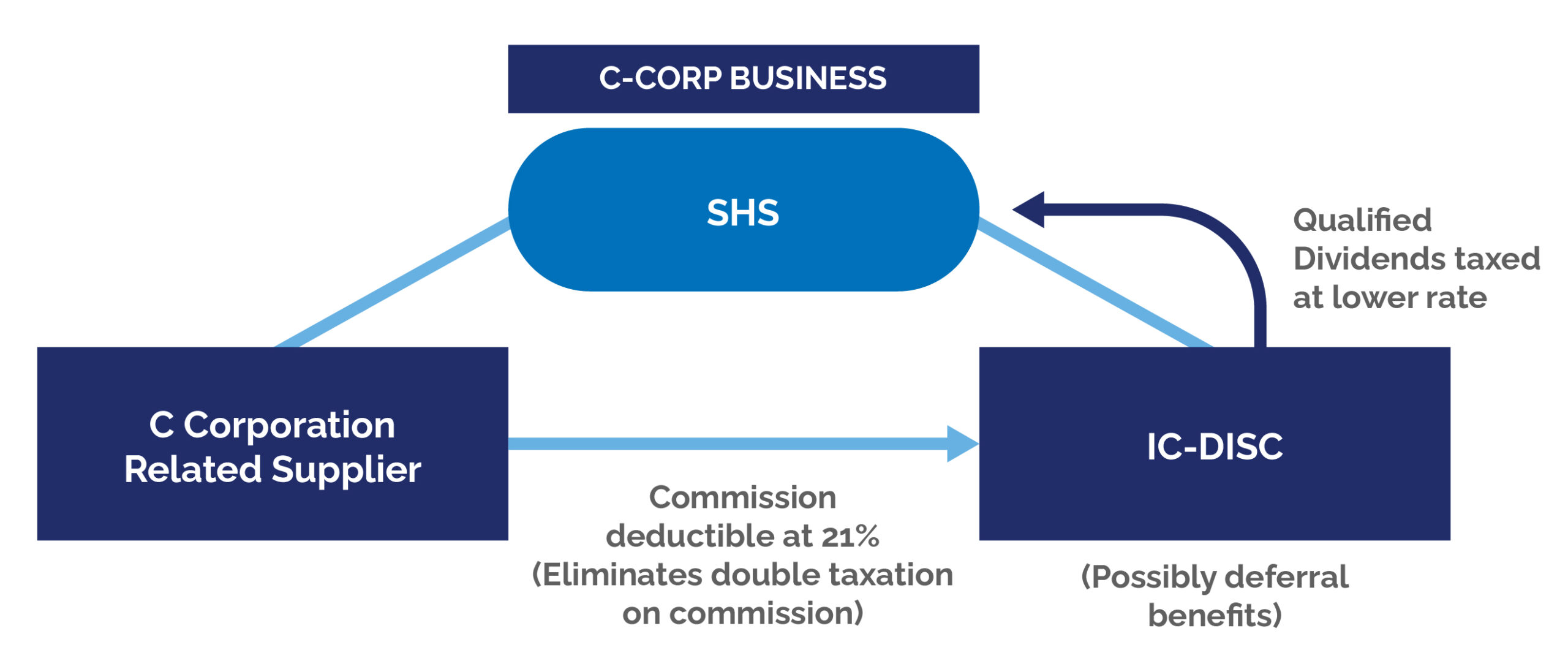

Companies can structure IC-DISC ownership in several ways; typically for pass-through entity structures, the partnership or S-corporation will directly own the IC-DISC. In C-corporation structures, typically the IC-DISC is brother-sister to the C-corporation operating company with the same or reasonably similar investor base.

How an IC-DISC Generates Tax Savings

The tax savings come from the following:

| Step | Operating/ Exporting Company | IC-DISC | Tax Effect |

| 1. Operating company (exporter) pays a commission to the IC-DISC | Deducts commission expense | Receives income tax-free | Reduces operating company/exporter ordinary income tax |

|

2. IC-DISC distributes dividends to shareholders as foreign source qualified dividend income |

N/A | Pays dividends to shareholders | Shareholders taxed at capital gain rates (i.e., 15-23.8% vs. up to 37%) generating permanent savings and possible foreign tax credit benefits |

Companies may also defer tax on up to $10 million of cumulative export income by holding earnings in the IC-DISC. The deferred tax is subject only to an interest charge based on the average 1-year Treasury bill rate. Accumulated amounts in excess of $10 million are deemed distributed and become previously taxed income that can be repatriated in the future.

For closely held businesses, including those operating through partnerships and S corporations, the IC-DISC structure is especially attractive. These structures often have the IC-DISC owned directly by the partnership or S corporation operating company. The commission payment by the business to the IC-DISC is potentially deductible at the partner/shareholder level at 37% (or if the partner/shareholder benefits from the QBI deduction at a 29.6% ETR). The IC-DISC pays no corporate level income tax on the commission income, and when paid to shareholders as qualified dividends, they pay a 23.8% maximum tax on the income. This results in a rate differential benefit for flow-through businesses ranging from 13.2% to 5.8%. This excludes any time-value of money deferral benefit if the IC-DISC retains income of $10 million or less.

Commission Calculation: Where the Real Strategy Lives

The tax code allows two main pricing methods for determining the commission paid to the IC-DISC:

- 4% of qualified export gross receipts, or

- 50% of combined taxable income (CTI) from export sales.

Businesses may choose whichever method produces the larger commission each year—which amounts to an annual opportunity to optimize the deduction. If done on a buy-sell basis (rare), then U.S. transfer pricing rules under section 482 are utilized.

Pricing Example:

- OpCo has $20 million in export sales (i.e., gross receipts);

- $5 million in net export income (i.e., CTI);

- The 4% gross receipts method yields a $800,000 commission; and

- The 50% CTI method yields a $2.5 million commission.

The company chooses the method which yields the higher commission, generating the maximum deduction for the operating business and therefore more tax savings. Higher margin businesses generally prefer the 50% of CTI method with lower margin businesses utilizing the 4% of gross receipts method.

While these are the two basic pricing methos, it is important to point out another method which is not often often recognized or utilized: the IC-DISC rules permit calculating the commission using a transaction-by-transaction (T-by-T) method or on product line grouping approaches to maximize the benefit.

Hyping of Benefits Through A/R Factoring

While the typical IC-DISC commission is based upon the 4% of export gross receipts or 50% of export CTI method, factoring allows an IC-DISC to achieve greater qualified income.

Where an operating company sells its receivables to an IC-DISC at a discount, these receivables constitute qualifying export assets supporting with IC-DISC qualification requirements and, with the right pricing, the income collected (while treated as interest income), is also considered qualifying export income. The operating company generates an ordinary tax deduction for a loss on the sale of the receivable (i.e., the A/R face value less discount), the total amount collected (presumably the face of the A/R in most cases) is eligible for income exemption and the qualified dividend rates. So, in effect, the benefit may be3 enhanced through this technique.

Many companies stop at commission planning, and factoring is a more sophisticated strategy involving valuation and transfer pricing specialists.

Qualification and Compliance Requirements

To maintain IC-DISC status each year, two eligibility tests apply to the corporation:

- 95% gross receipts test: At least 95% of the IC-DISC income must come from qualified export receipts; and

- 95% asset test: At least 95% of the IC-DISC assets must be qualified export assets (which include receivables tied to export sales).

Failure of either test can disqualify the IC-DISC, eliminating tax benefits.

Additionally, IC-DISCs must:

- Maintain their own accounting records;

- Keep a separate bank account; and

- File Form 1120-IC-DISC (typically due September 15 for calendar-year entities).

These compliance obligations are minimal but not optional. We generally recommend an annual compliance and documentation review prior to year-end to validate the ongoing status and the commission to be accrued.

When IC-DISCs Make Strategic Sense

IC-DISCs deliver the strongest return for exporters that:

- Maintain consistent export sales (generally, at least $2 million or more annually);

- Have strong margins on international orders; and

- Expect ongoing growth in foreign markets.

They can also facilitate:

- Working capital loans from the IC-DISC to the operating company that generates qualifying export income;

- Incentive compensation programs tied to export performance by allowing key employees ownership interests; and

- Estate- and succession-planning structures (e.g., value freezes).

From a financial planning perspective, the IC-DISC functions not only as a tax strategy, but as a broader tool to support capital efficiency and organizational strategy.

Why IC-DISCs Still Matter Today

Even after the TCJA reform lowered corporate tax rates for 2018 forward, IC-DISCs remain relevant because the benefit is not tied to corporate tax—it is tied to rate arbitrage between ordinary income and qualified dividends.

With respect to C corporations with a 21% corporate tax rate, there can still be benefits because the amount of the commission deduction avoids double taxation at the corporate level and capital can be redeployed through producer’s loans and some deferral obtained where export profits do not exceed $10M cumulatively. That said, the TCJA corporate rate reduction has cut the benefit to C corporation taxpayers significantly, especially with shareholders subject to the NII tax.

In short, for flow-through businesses the:

- Ordinary income rate can be as high as 37%; and the

- Qualified dividend rate is typically 15–23.8%.

That differential represents a permanent tax benefit.

IC-DISCs are, in effect, the last remaining export incentive available to U.S. manufacturers and exporters, other than the section 250 foreign derived intangible income (FDII) deduction (which only applies to domestic C corporations). The FDII regime has broader application, but the benefit can be limited by losses, the relative amounts of income between U.S. and foreign markets, and profit margins.

Conclusion

For U.S. exporting businesses, the IC-DISC offers a rare combination of characteristics:

- No operational disruptions to implement or maintain;

- High operational certainty with a large body of law;

- Significant permanent tax savings in the right circumstances; and

- Strategic uses for capital, compensation, and succession planning depending on the taxpayer’s facts.

Particularly for flow-through businesses that export U.S.-made goods and certain services, the question is no longer whether we should explore an IC-DISC, but that it should be a strategic imperative.

If you need personalized guidance, connect with our international tax services team here or connect with our transfer pricing services team here.

Our International Tax Services Team

Scott Montopoli

Senior Director, International Tax Services

Tyler LeFevre

Senior Manager, International Tax Services

Jonathan Voll

Director, Transfer Pricing Services